United States

United States Australia

Australia

Posted on: 12/09/2023

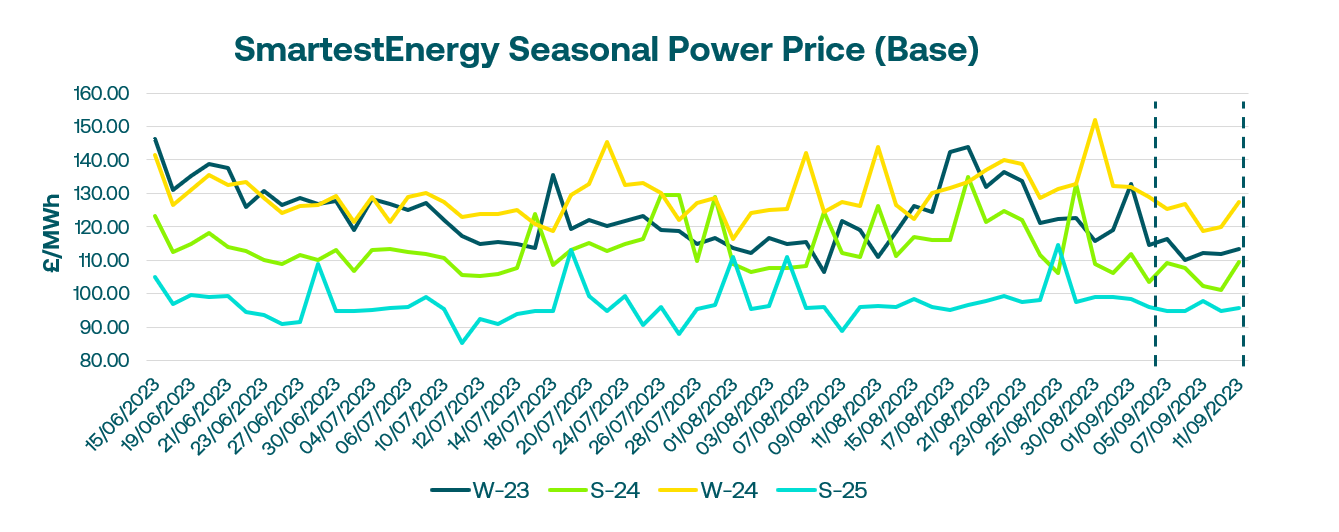

Head of Sales Trading, Fanos Shiamishis, reports on energy market activity, covering the period 5th September – 11th September 2023. On our end-of-day pricing tool, The Source, we published an in-week high of £116.38/MWh for the Winter-23 seasonal power price on 5th September. In this blog, Fanos shares the market news and updates from the last week.

On 5th September European gas prices remained stable as mediation talks, facilitated by the Fair Work Commission, continued while Chevron's Gorgon and Wheatstone LNG sites brace for brief stoppages. It was announced that if an agreement on pay and working conditions isn't reached, workers may initiate a two-week total strike beginning on 14th September. Meanwhile, the UK gas system experienced a shortage due to reduced LNG sendout and the return of some Norwegian fields from maintenance. Liquidity in the UK power market remained limited, with only 15MW of front season baseload trading activity.

On Wednesday, the UK gas system experienced a deficit of 16mcm. Initially, NBP prices saw an increase in the morning, but they later decreased as the LNG strike in Australia was postponed until Friday, allowing for extended negotiation time. UK power prices declined on Wednesday afternoon, and there was limited interest from buyers.

On 7th September European gas markets experienced fluctuations once more as the anticipated Chevron Australia LNG strike faced a 7-hour delay. However, reaching an agreement remained unlikely. The UK gas system started the day in a deficit, primarily attributed to a 1mcm/d reduction in Langeled nominations owing to the extended Troll and Kollsnes outage. LNG deliveries to the UK remained limited, with only one vessel expected by the end of the month. On the other hand, front-month UK power trading showed high liquidity.

The market reacted swiftly as reports of a breakdown in mediation talks at Chevron's Australian LNG operations emerged around 10 am on Thursday. This led to a general uptrend in market activity, with potential substantial price fluctuations over the weekend. This was a contrast to Wednesday's news confirming the postponement of strikes during ongoing mediation talks. Although the fundamental supply situation remained robust, the risk premium associated with the LNG industrial action continues to exert a notable influence on front-month prices.

Chevron are now seeking a resolution through an industrial adjudicator. Australian tribunal has set a dispute hearing for 22nd September, but it is expected to take a few weeks to progress to a complete resolution. This new legislation has not been put to the test yet, so if Chevron successfully halts the strike through the adjudicator, it would set a significant legal precedent. No further negotiation talks have been planned with the workers.