Smartest Insight | Issue 92

![]()

Our weekly company round-up covers the key market and industry news in one place, so you don’t have to look any further to stay ahead.

August 18, 2022

MARKET UPDATE:

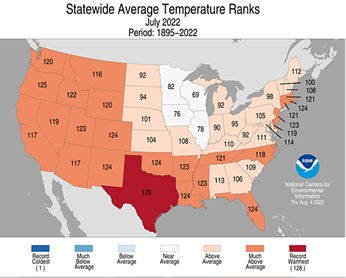

Natural gas futures are up over$1.50/MMBtu over the past week amid production declines and European power and gas markets continue to hit all time highs. The EIA is expected to Report an injection of 35 Bcf for the week ending August 12th. If that is the case the deficit to the five-year-average would increase to 350 Bcf (12% below the average). The strong summer demand from the power sector has been the main contributing factor to the deficit. Nationally, July was the third hottest July on record dating back 128 years with Texas experiencing the hottest month ever (graph right).

Power prices have rebounded sharply but are still off of the highs that we saw the May-June timeframe, suggesting that there is still room to the upside.

EIA SHORT TERM OUTLOOK

The U.S. Energy Information Administration (“EIA”) released its short-term outlook on August 9, 2022. Key highlights for natural gas are as follows:

- EIA expects Henry Hub prices to average $7.54/mmBtu in the second half of 2022 and then fall to an average of $5.10/mmBtu in 2023 amid rising natural gas production. 2023 Henry Hub futures currently average about $6.10/mmBtu.

- In July, Henry Hub spot prices averaged $7.28/mmBtu, down from $7.70/mmBtu in June. Average natural gas prices fell primarily due to added supply resulting from the shutdown of Freeport’s 2Bcf/d LNG export terminal on June 8. However, prices increased materially throughout July (from $5.73/mmBtu on July 1 to $8.37/mmBtu on July 29), because of continued high power plant demand due to scorching temperatures throughout the U.S.

- U.S. natural gas inventories ended July at 2.5 Tcf, which was 12% below the 2017–2021 average. EIA estimates that natural gas inventories will end the 2022 injection season 3.5 Tcf, which would be 6% below the five-year average. (end of October) at close to

- EIA estimates that U.S. LNG exports will average 10.0 Bcf/d in 3Q22 and 11.2 Bcf/d for all of 2022, a 14% increase from 2021. This increase is the result of additional export projects that have come online and Freeport LNG resuming operations sooner than we had initially expected. EIA forecasts that LNG exports will average 12.7 Bcf/d in 2023. EIA also noted that in early 2022, the United States became the largest LNG exporter in the world.

- EIA forecasts that U.S. natural gas consumption will average 85.2 Bcf/d in 2022 (up 3% from 2021) and 83.8 Bcf/d in 2023 (down 2% from forecasted 2022).

- EIA estimates that U.S. dry natural gas production will average 97.1 Bcf/d in August, 96.6 Bcf/d during all of 2022, and 100 Bcf/d in 2023.

NYSERDA TIER 2 RFP

On August 16, 2022, the New York State Energy Research & Development Authority (“NYSERDA”) announced a competitive Tier 2 REC solicitation under which NYSERDA will purchase Tier 2 RECs rom eligible York state that entered commercial operation prior to January 2105. NYSERDA’s Tier 2 program is designed to offer incentives to remain operational to those renewable projects that do not qualify for Tier 1 REC payments. Proposals are due by September 15, 2022. NYSERDA is expected to begin paying awarded generators on January 1, 2023. NYSERDA charges the costs of Tier 2 RECs to electricity suppliers, who pass the costs onto customers.