United States

United States Australia

Australia

Posted on: 31/01/2023

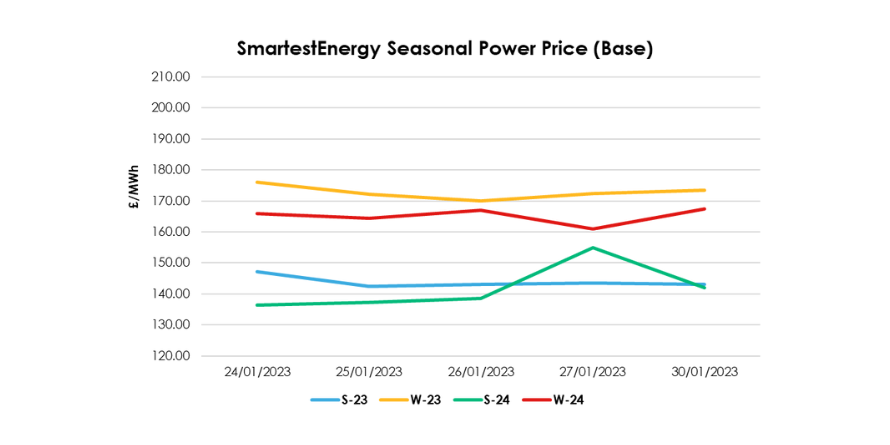

Head of Sales Trading, Fanos Shiamishis, reports on the energy market activity, covering the period 24th – 31st January 2023. On our end-of-day pricing tool, the Source, we published an in-week high of £147.15/MWh for the Summer-23 seasonal power price on 24th January, reducing to £143/MWh yesterday. In this blog, Fanos shares the market news and updates from the last week.

Last week, gas prices declined and traded in a smaller range. Both NBP and TTF were down amid higher wind output and milder, warmer weather forecasts leading to lower gas for power demand. Forward prices also lowered due to news of Freeport LNG, the second largest US exporting facility, completing repairs, and requesting regulatory clearance to restart the facility.

The UK’s Dirty Spark Spread widened on Thursday with gas prices softening out to Winter 23 whilst power traded flat the previous day. Sellers came out in force later in the day, but the Clean Spark Spread held value due to strong Carbon prices (EUA and UKA).

On Friday, markets opened soft in the morning with the fundamental drivers showing no strain on supplies. The trend reversed by 3pm with near dated contracts reverting against the latest demand forecasts and short positions across TTF, NBP and Baseload closing out ahead of contract expiry. Prices are still lower by around 20% week on week.

With the gas February 23 contract expiring yesterday and power expiring today, February opened stronger than last week with the opening trades registering at £143/MWh. Additionally, the UK gas system opened short yesterday with Norwegian field outages cited as the main supply squeeze. Later in the day, weather and demand fundamentals prevailed with a mild February forecasted, higher wind and minimal probability of a cold spell adding confidence to a well-supplied February.