United States

United States Australia

Australia

Posted on: 07/03/2023

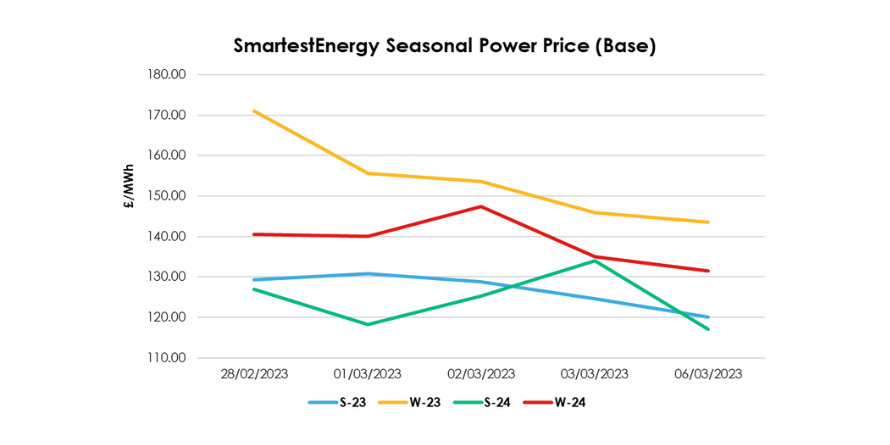

Head of Sales Trading, Fanos Shiamishis, reports on the energy market activity, covering the period 28th February – 7th March 2023. On our end-of-day pricing tool, the Source, we published an in-week high of £130.75/MWh for the Summer-23 seasonal power price on 1st March, reducing to £120.01/MWh yesterday. In this blog, Fanos shares the market news and updates from the last week.

Last week, prices continued to reduce with the UK System opening 30mcm long on Tuesday morning. The latest gas demand forecasts remain around 20mcm below seasonal average expectation. February’s summary report indicates that Gazprom exports to Europe rose by 16% during February.

Prices rose slightly on Wednesday amid higher demand for heating. However, high inventory level and healthy supply flow are limited gains. The UK gas system was long in the morning with Norwegian gas flows up and lower wind output. Both gas and power are traded in a narrow range.

European gas traded in a tight range on Thursday on strong supply and healthy storage levels that offset strong demand due to lower than normal temperatures. A French lower house committee has passed amendments to draft legislation which would scrap the target to cut the share of nuclear power in the country’s power mix to 50% by 2035, it also removes the existing 62.3GW cap on French nuclear capacity.

Last week ended with a strong LNG shipment schedule to UK and Europe and milder temperatures forecasted. European gas stores are currently at 60.62%. Any hopes of long-term energy stabilisation in a post conflict Europe also seem to be waning with Gazprom announcing the sealing and mothballing of the Nord Stream 1 and 2 pipelines.

Gas storage levels hit above a ten-year average of 39%. UK gas system was short yesterday morning and Norwegian flow was slightly down as well as nominated LNG sendout. There is no Interconnector UK export until 8th March due to an unplanned outage.