United States

United States Australia

Australia

Posted on: 10/01/2023

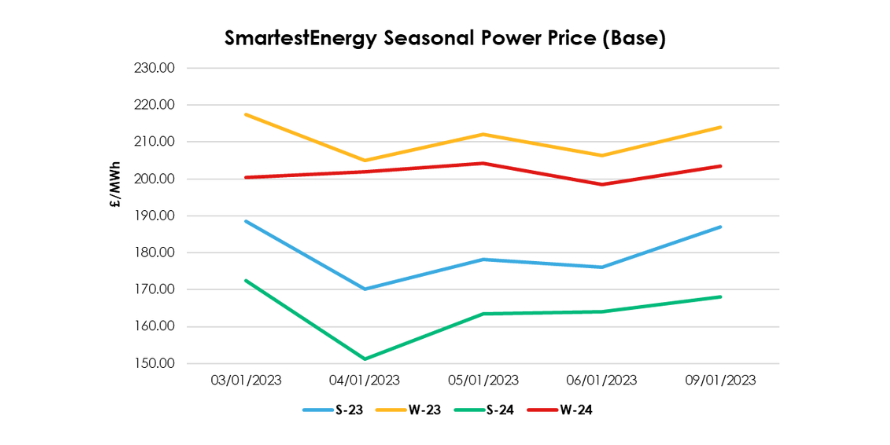

Head of Sales Trading, Fanos Shiamishis reports on the energy market activity, covering the period 3rd – 10th January 2023. On our end of day pricing tool, the Source, we published an in week high of £188.50/MWh for the Summer-23 seasonal power price on 3rd January reducing to £187/MWh yesterday. In this blog Fanos shares the market news and updates from the last week.

Last week, despite the UK gas system opening short, demand remained low and domestic supplies high. The significant draw on UK system were exports and forward supplies seemed strong whilst demand remains unchanged and below seasonal normal expectations. Continental demand forecasts edged lower, adding further bearish sentiment to the market.

Further softening amid warmer weather, strong renewable output and ample LNG supply resulted in weaker energy prices. Colder weather and lower wind were expected in parts of Europe later last week.

Most of UK power activity was focused on front month, quarter and seasonal with Summer 23 trading 304MW in total on 5th January. It was reported that French Nuclear output fell 23% year on year to 279 TWh in 2022, its lowest level since 1989 mainly due to maintenance delays and corrosion issues causing unplanned reactor outages. Norwegian gas flows were up, while LNG send out was lower on 6th January. Strong winds were potentially preventing cargo unloading at South Hook LNG terminal.

Yesterday saw prompt gas prices rise with colder temperatures forecasted and high winds impacting freight, leading to low LNG send out. Although the expected increase in gas demand for heating is driven by the colder temperatures, we have seen some offsetting in gas demand for power generation via the forecasted higher wind generation. Gas supplies across Europe reinforced by high storage levels abating some of the LNG send out risk caused by high winds.